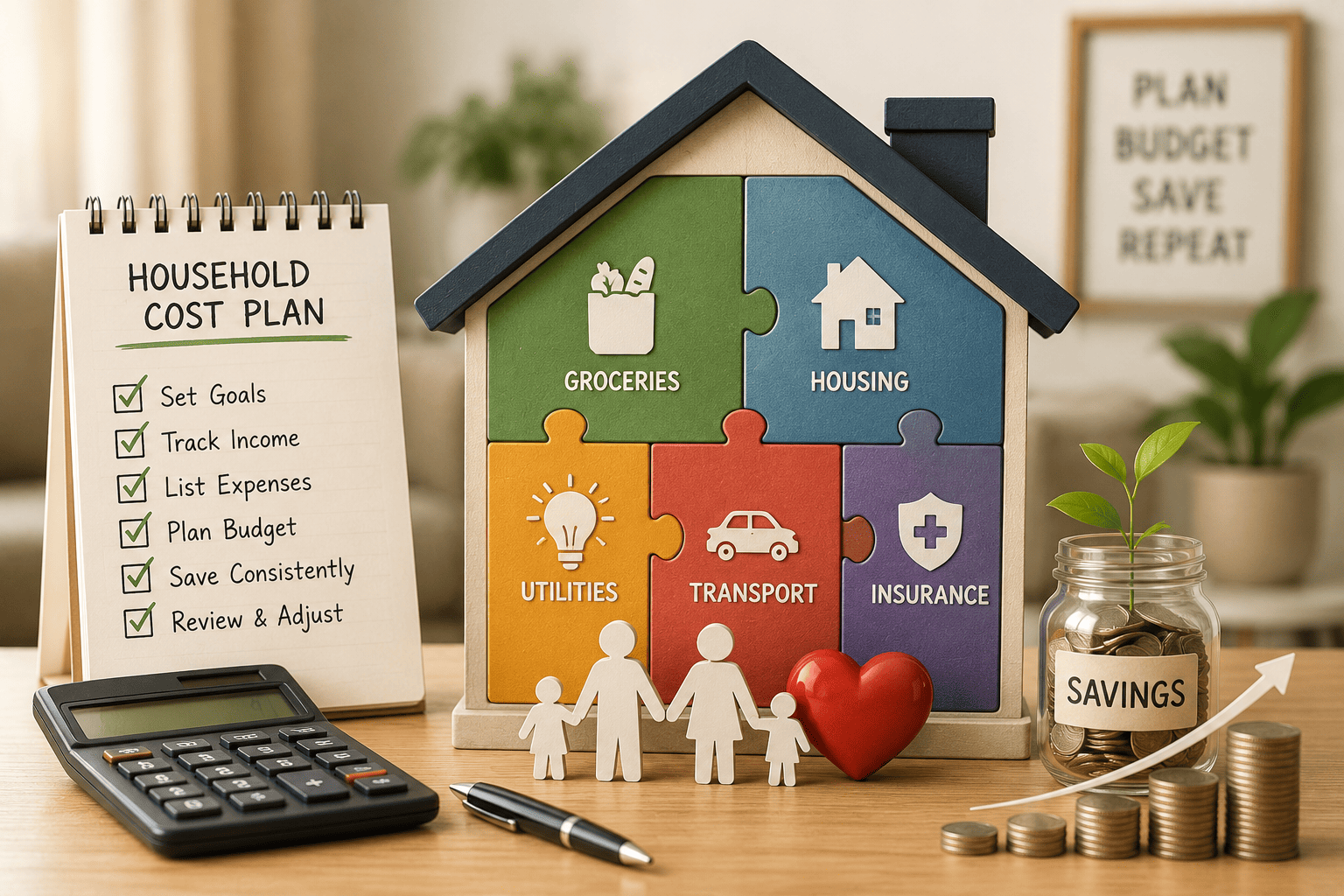

Most budgets fail because they are too complicated to maintain. A household cost plan is different: it is a simple map of where your money goes each month, built so you can actually keep using it. The bonus is that a clear map makes it obvious where a Support System could close a gap.

Step 1: List Your Fixed Costs

Start with the bills that stay roughly the same every month — rent or mortgage, utilities, insurance, phone, and any loan payments. These are predictable, which makes them the easiest place to spot a program that could lower a recurring cost.

Step 2: Estimate Your Variable Costs

Next, add the costs that move month to month: groceries, transportation, healthcare, and household supplies. You do not need exact numbers — a reasonable monthly average is enough to see the shape of your spending.

The gap is where Support Systems help

When your essential costs come close to or exceed your income, that difference is the "gap." Support Systems are designed to reduce specific costs — energy, healthcare, housing, food — so the clearest path is to match each gap to the category built to close it.

Step 3: Match Gaps to Programs

Once your costs are mapped, look at the biggest line items and ask which category of Support System addresses them:

- High energy bills → energy and utility programs.

- Healthcare costs → Marketplace, Medicaid, or clinic programs.

- Housing pressure → rental or property-tax offset programs.

Step 4: Keep It Simple So It Lasts

Review your plan once a month, not once a day. A short, regular check-in keeps the plan alive and helps you notice when a new program might apply. Our free Household Cost Gap Analyzer can do this matching automatically.

Step 5: Build a Small Buffer Before Anything Else

Before refining anything, give your plan a cushion. A buffer does not have to be large to be powerful — even a modest amount set aside changes how the whole plan feels, because it absorbs the small surprises that otherwise force you into a bill you cannot pay. Think of it less as savings and more as shock absorption. When a car repair or a higher-than-usual utility bill lands, the buffer takes the hit instead of your rent, and the plan keeps running without a crisis.

The simplest way to build one is to treat it as a fixed cost. Add a small, recurring line to your plan labeled “buffer” and fund it like any other bill, even if it is only a little each month. The goal is not a specific number; it is the habit of always having something between you and the next surprise.

Needs and Wants Without the Guilt

A useful cost plan separates needs from wants, but it does so without shame. Needs are the costs that keep your household safe, housed, fed, warm, and able to earn — housing, utilities, basic food, transportation to work, essential healthcare. Wants are everything that improves life but could pause for a month without harm. The point of the line is not to eliminate wants; it is to know which costs you could flex if you ever needed to, so that in a tight month you make calm choices instead of panicked ones.

Be honest but kind in how you sort. A small, regular comfort that keeps you steady is not a frivolous expense; it is part of being able to maintain the plan at all. The aim is clarity, not austerity.

A Simple Structure That Survives Real Life

Many households find it easier to manage money in a few broad buckets rather than dozens of tiny categories. One common approach is to think in three groups: essentials, flexible spending, and a future bucket that holds both your buffer and any goals. You do not need exact percentages — you need a structure simple enough that you can keep using it when life gets busy. The fewer moving parts a plan has, the more likely it survives a stressful week.

- Essentials — the costs that keep the household running.

- Flexible — the spending you can dial up or down month to month.

- Future — your buffer first, then any longer-term goals.

Tracking Without Spreadsheets

You do not need complicated software to run a cost plan. The most reliable method is the one you will actually keep doing. For some people that is a note on the fridge; for others it is a banking app that sorts spending automatically; for others it is a single page reviewed on the same day each month. What matters is consistency, not sophistication. A rough plan you maintain beats a perfect plan you abandon after two weeks.

The monthly fifteen-minute review

Pick one day a month and give your plan fifteen minutes. Compare what you expected to spend with what you actually spent, adjust one or two numbers, and check whether any large bill is approaching. That short, regular habit is what keeps a cost plan accurate — and it is usually where you spot a gap a Support System could close.

Seasonal Costs People Forget

Budgets often break not on the predictable monthly bills but on the costs that arrive a few times a year — higher heating or cooling bills in extreme seasons, school-related expenses, insurance premiums billed annually, holidays, and routine car maintenance. Because these costs are irregular, they feel like surprises even though they happen every year. The fix is to spread them out: estimate the yearly total, divide by twelve, and set that amount aside monthly so the bill is already covered when it lands.

Seasonal energy costs are worth special attention, because they are both predictable and often the largest swing in a household budget. Planning for them in advance is also what makes energy assistance programs easy to slot in when they apply, since you already know roughly what the season will cost.

Matching Each Cost Category to the Right Support System

One of the quiet benefits of a clear cost plan is that it turns “I need help” into a precise question. Instead of searching broadly, you can look at your largest lines and aim straight at the category built to lower them:

- Energy and utilities — for high heating, cooling, or electricity costs.

- Healthcare — Marketplace, Medicaid, or community clinic programs for medical lines.

- Housing — rental support or property-tax offsets when shelter is the heaviest cost.

- Food and nutrition — programs that lower grocery spending for qualifying households.

- Tax offsets — credits that return money at filing time and can be planned for in advance.

Adjusting the Plan When Income Changes

A cost plan is not a monument; it is a living tool. When income rises or falls — a new job, reduced hours, a seasonal change in work — revisit the plan within a week rather than waiting for the next month. Update your essentials first, protect the buffer if you can, and trim flexible spending before touching needs. A plan that bends with your income is one that never breaks, and a recent income change is also the perfect moment to re-check which Support Systems you now qualify to explore.

Common Budgeting Mistakes to Avoid

- Making it too detailed. A plan with fifty categories is a plan you will stop updating. Keep the buckets broad.

- Forgetting irregular costs. Annual and seasonal bills sink more budgets than daily spending ever does.

- Skipping the buffer. Without a cushion, a single surprise cascades into late fees and missed bills.

- Reviewing too often or never. Daily checking burns you out; never checking lets the plan drift. Once a month is the sweet spot.

A household cost plan is ultimately a way to replace worry with information. When you can see where your money goes, the gaps stop being vague anxieties and become specific, solvable problems — and many of those gaps line up exactly with the Support Systems built to close them.

Putting Your Plan on Paper for the First Time

If you have never written a cost plan before, the hardest part is simply starting, so make the first version deliberately rough. Take a single sheet of paper or open one note, and write your monthly income at the top. Below it, list your fixed costs, then your variable costs, then your buffer. Subtract the total from your income. Whatever number you get — positive or negative — is your starting point, and it is far more useful than a perfect plan you never begin. You can refine the figures next month; the goal of the first pass is only to see the whole picture in one place.

Do not worry about getting every number exactly right. Estimates are fine, and they get more accurate naturally as you review the plan over the months. A plan that exists and is roughly correct will always serve you better than an exact one that lives only in your head.

When the Numbers Do Not Add Up

Sometimes the first plan shows your essential costs sitting close to or above your income. This is uncomfortable to see, but it is also exactly the moment the plan earns its keep, because now the problem is specific instead of vague. When costs outrun income, work the problem in a calm order: protect the true essentials first, look for the single largest cost you might lower, and match that cost to the category of Support System designed for it. A housing line that is too heavy points toward housing or property-tax programs; a punishing energy bill points toward energy assistance; high medical costs point toward healthcare support.

Seeing a shortfall on paper is not a failure; it is information you can act on. Most households that close a gap do so by addressing one or two large costs rather than a dozen small ones, and a clear plan is what shows you which costs those are.

Talking About Money in a Household

If more than one person shares the household, the plan works best when it is shared too. Money is a sensitive subject, so keep the conversation focused on the plan rather than on blame. Walk through the same page together, agree on which costs are essential, and decide as a group where the flexible spending can move in a tight month. When everyone can see the same map, decisions stop feeling like arguments and start feeling like teamwork. A plan that the whole household understands is also far more likely to survive, because no single person is carrying it alone.

The Long-Term Payoff of a Simple Plan

The real reward of a household cost plan is not a single solved month; it is the steady confidence that comes from always knowing where you stand. Over time, the monthly review becomes second nature, the buffer grows, and the surprises that once felt like emergencies become manageable bumps. Just as importantly, you develop a trained eye for the moments when a Support System could help — a rising energy bill, a new medical cost, a change in income — and you can act on them early. A simple plan, kept faithfully, turns money from a source of worry into a tool you control.

Start small, keep it simple, and review it on the same day each month. That is the entire method, and it is enough. A household cost plan does not ask you to be perfect with money; it only asks you to look at it honestly and regularly. From that single habit, everything else — the buffer, the closed gaps, the calmer months — quietly follows.

Remember that a plan is meant to serve you, not the other way around. If a method feels too heavy, simplify it until it fits your life, because the only plan that helps is the one you actually keep. Begin with a single honest page this week, return to it next month, and let it grow with you. That steady, forgiving rhythm is what carries a household from worrying about money to quietly managing it.

The rest of this guide is for Members

You've read the first half free. Unlock the full guide to keep reading the remaining steps, checklists, and details.

Unlock With Member